White Box Server Market: Powering the Next-Gen Data Center Economy (2024–2030)

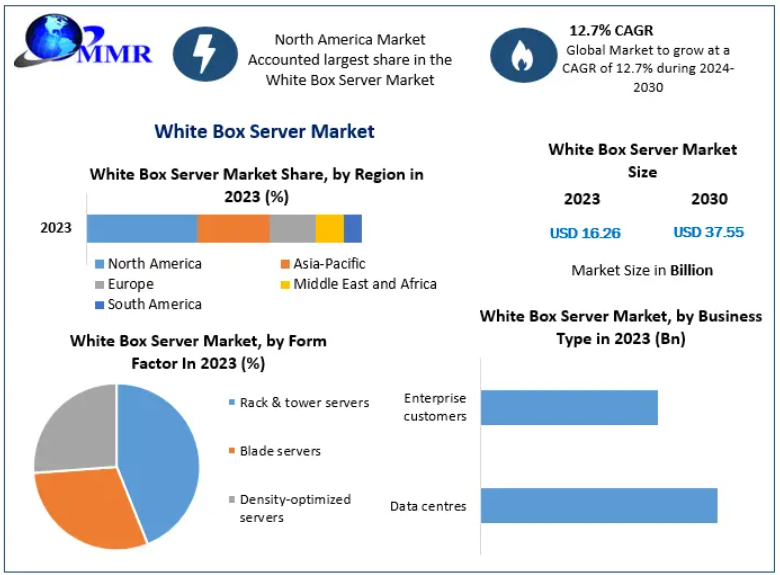

The global White Box Server Market is rapidly transforming the data center landscape, driven by the demand for cost-efficient, customizable, and high-performance computing infrastructure. The market, valued at USD 16.26 billion in 2023, is projected to reach USD 37.55 billion by 2030, expanding at a robust CAGR of 12.7%.

Market Overview

White box servers are non-branded, customizable servers built by original design manufacturers (ODMs) rather than traditional OEM brands. These servers are widely used in hyperscale data centers, cloud environments, and enterprise IT infrastructure due to their flexibility and cost advantages.

Unlike branded servers, white box systems allow organizations to tailor hardware configurations according to specific workloads—making them ideal for big data, AI, and cloud computing applications.

For further information, click the following link:https://www.maximizemarketresearch.com/request-sample/65959/

Key Growth Drivers

- Explosion of Data Centers

The surge in global data generation, fueled by cloud computing, IoT, and AI applications, has led to a massive increase in data center deployments. Hyperscale operators are increasingly adopting white box servers for scalability and cost optimization.

- Adoption by Tech Giants

Major internet companies like Meta Platforms, Inc. (Facebook) and Google LLC are key adopters of white box servers. These organizations prefer customized hardware solutions to efficiently manage massive workloads.

- Open Compute Movement

Initiatives like the Open Compute Project (OCP) are promoting open hardware designs, encouraging enterprises to move away from proprietary systems and adopt flexible, standardized server architectures.

- Cost Efficiency & Customization

White box servers offer significant cost savings compared to branded alternatives. Their modular design enables easy upgrades, simplified maintenance, and optimized performance for specific applications.

Market Challenges

Reliability Concerns

Compared to branded servers, white box servers may face challenges related to redundancy, reliability, and support services, particularly in smaller deployments without strong IT expertise.

Limited Vendor Support

The absence of a single vendor ecosystem can create integration and maintenance challenges for enterprises lacking technical resources.

Segment Analysis

By Form Factor

- Rack & Tower Servers dominate the market due to widespread adoption in enterprise IT infrastructure.

- Density-Optimized Servers are the fastest-growing segment, designed for hyperscale data centers with high computing density and energy efficiency.

- Blade Servers offer compact and scalable solutions for specialized environments.

By Business Type

- Data Centers represent the fastest-growing segment, driven by cloud providers and large-scale enterprises.

- Enterprise Customers are increasingly adopting white box servers for cost-effective IT infrastructure.

By Processor

- X86 Servers dominate due to compatibility with most enterprise workloads.

- Non-X86 Servers are gaining traction in specialized computing environments.

By Operating System

- Linux-based systems lead the market due to their open-source flexibility and compatibility with white box architectures.

- Other systems include Windows and UNIX-based platforms.

For further information, click the following link:https://www.maximizemarketresearch.com/request-sample/65959/

Regional Insights

- North America leads the global market, supported by a high concentration of data centers and strong adoption by cloud service providers.

- Asia-Pacific is emerging as a high-growth region, driven by digital transformation in countries like China, India, and Japan.

- Europe is witnessing steady growth due to increasing investments in cloud infrastructure and data sovereignty initiatives.

- Middle East & Africa and South America are gradually expanding with rising IT infrastructure investments.

Competitive Landscape

The white box server market is highly competitive, with ODMs and system integrators focusing on innovation, scalability, and cost leadership. Key players include:

- Quanta Computer Inc.

- Wistron Corporation

- Inventec Corporation

- Hon Hai Precision Industry Co., Ltd.

- Celestica Inc.

- Super Micro Computer, Inc.

- ZT Systems

These companies are heavily investing in high-density computing, AI-ready servers, and energy-efficient designs to meet evolving enterprise demands.

Emerging Trends

- AI and High-Performance Computing (HPC) workloads driving demand for customized servers

- Edge computing adoption requiring compact and scalable white box solutions

- Sustainability focus with energy-efficient server architectures

- Integration with cloud-native technologies like Kubernetes and containerization

Future Outlook

The future of the white box server market is closely aligned with the growth of cloud computing, AI, and big data ecosystems. As enterprises continue to prioritize flexibility and cost efficiency, white box servers will play a crucial role in shaping next-generation IT infrastructure.

By 2030, the market is expected to be dominated by hyperscale deployments, open hardware ecosystems, and AI-driven server optimization, making white box servers a cornerstone of the global digital economy.